Mean Squared Error: In and Out of Sample

Use data to learn a model. What does that mean?

Begin with some data. Assume a linear model.

![]()

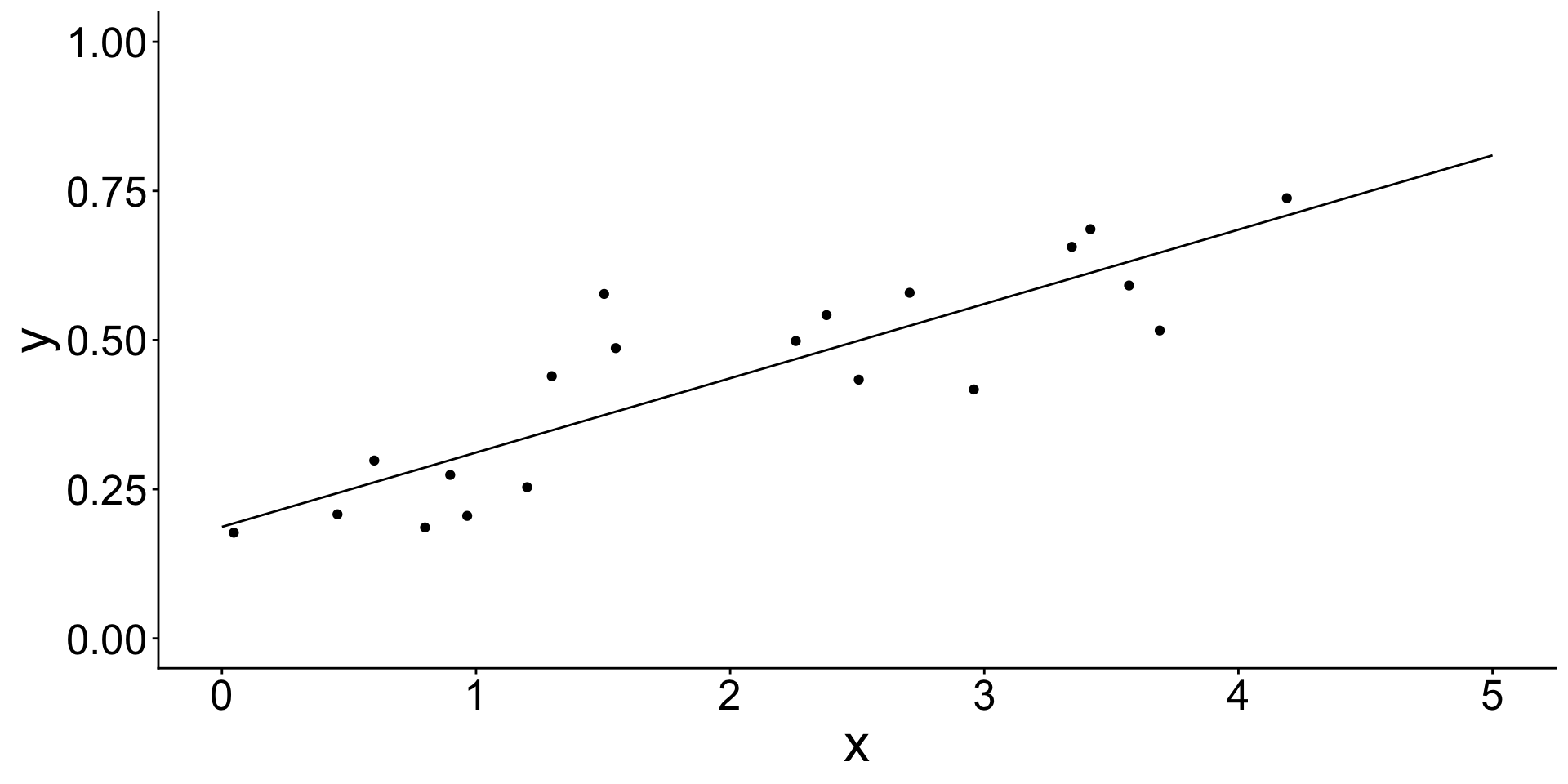

Estimate a linear model

Call:

lm(formula = y ~ x, data = simulated)

Residuals:

Min 1Q Median 3Q Max

-0.138289 -0.069877 0.006674 0.056056 0.203069

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.18696 0.03969 4.71 0.000175 ***

x 0.12455 0.01688 7.38 7.58e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.09133 on 18 degrees of freedom

Multiple R-squared: 0.7516, Adjusted R-squared: 0.7378

F-statistic: 54.47 on 1 and 18 DF, p-value: 7.578e-07

Estimate a linear model

![]()

The model learned coefficient values from the data.

![]()

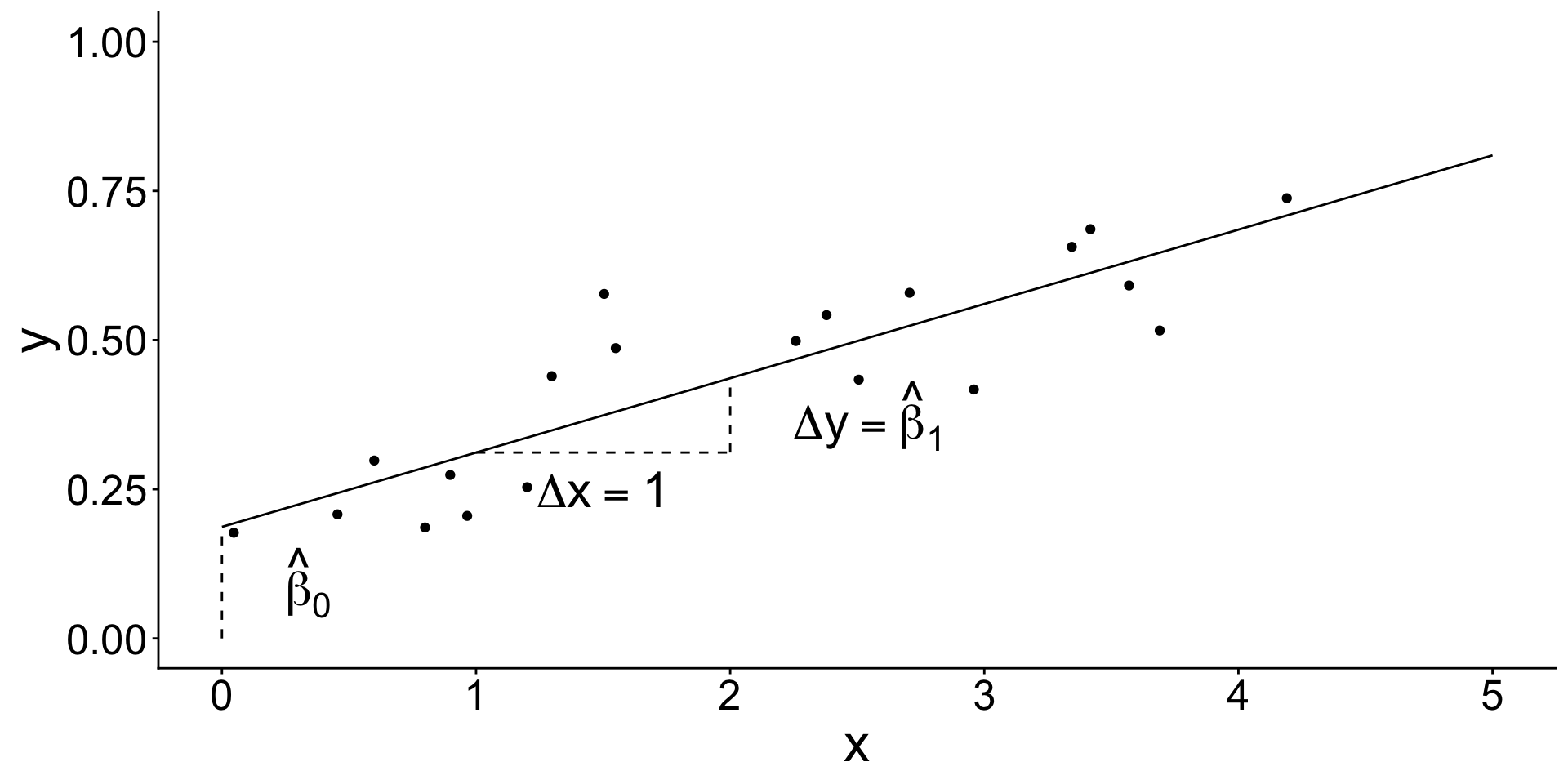

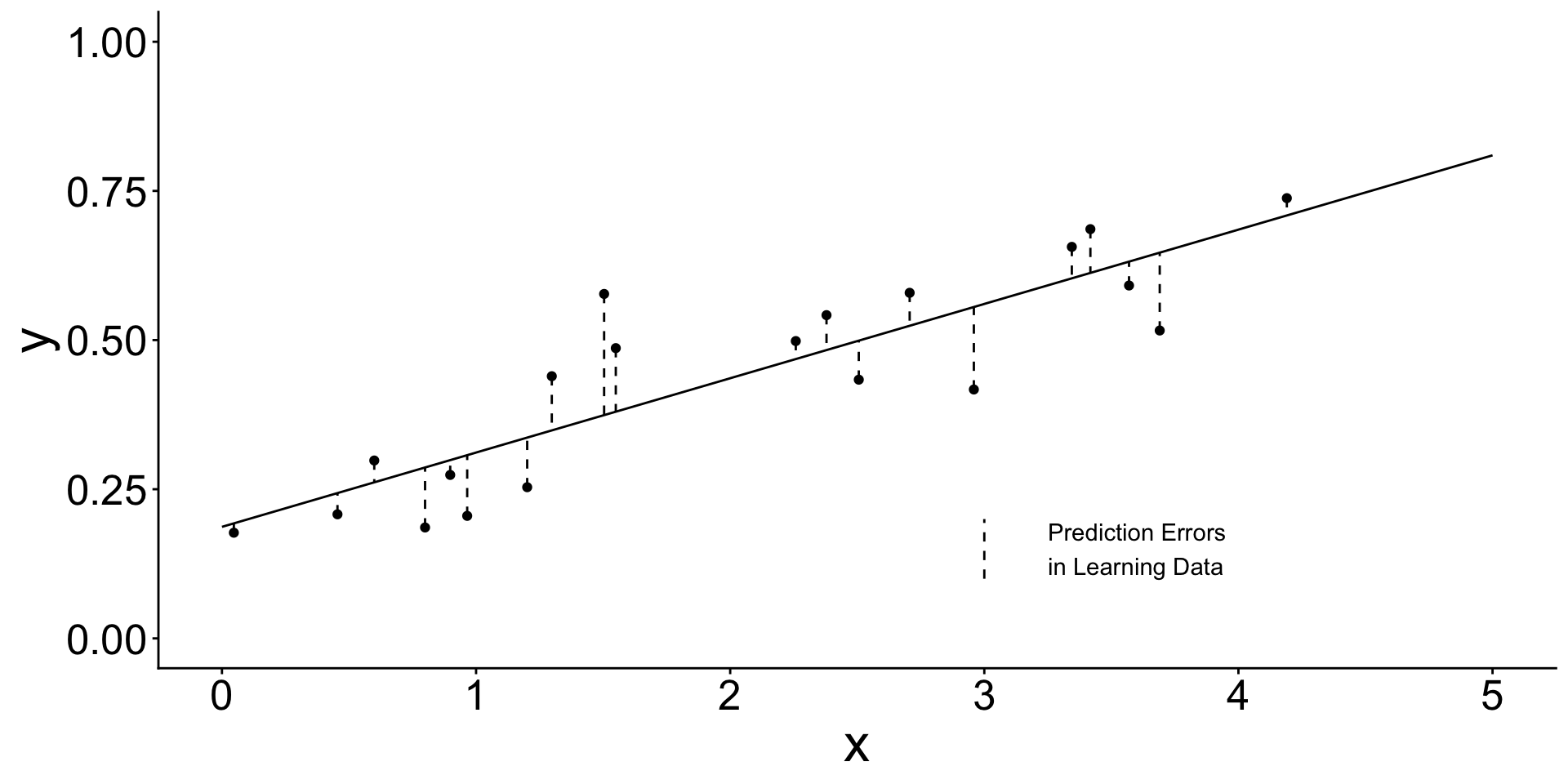

How? It learned by minimizing the sum of squared errors

![]()

How? It learned by minimizing the sum of squared errors

\[

\begin{aligned}

\text{Sum of squared error:}\qquad &\sum_{i\in\text{learning}} \left(y_i - \hat{y}_i\right) ^ 2 \\

\text{Mean squared error:}\qquad &\frac{1}{n_\text{Learning}}\sum_{i\in\text{learning}} \left(y_i - \hat{y}_i\right)

\end{aligned}

\]

- We estimated the line in

learning data

- Now we evaluate the estimated line in

testing data

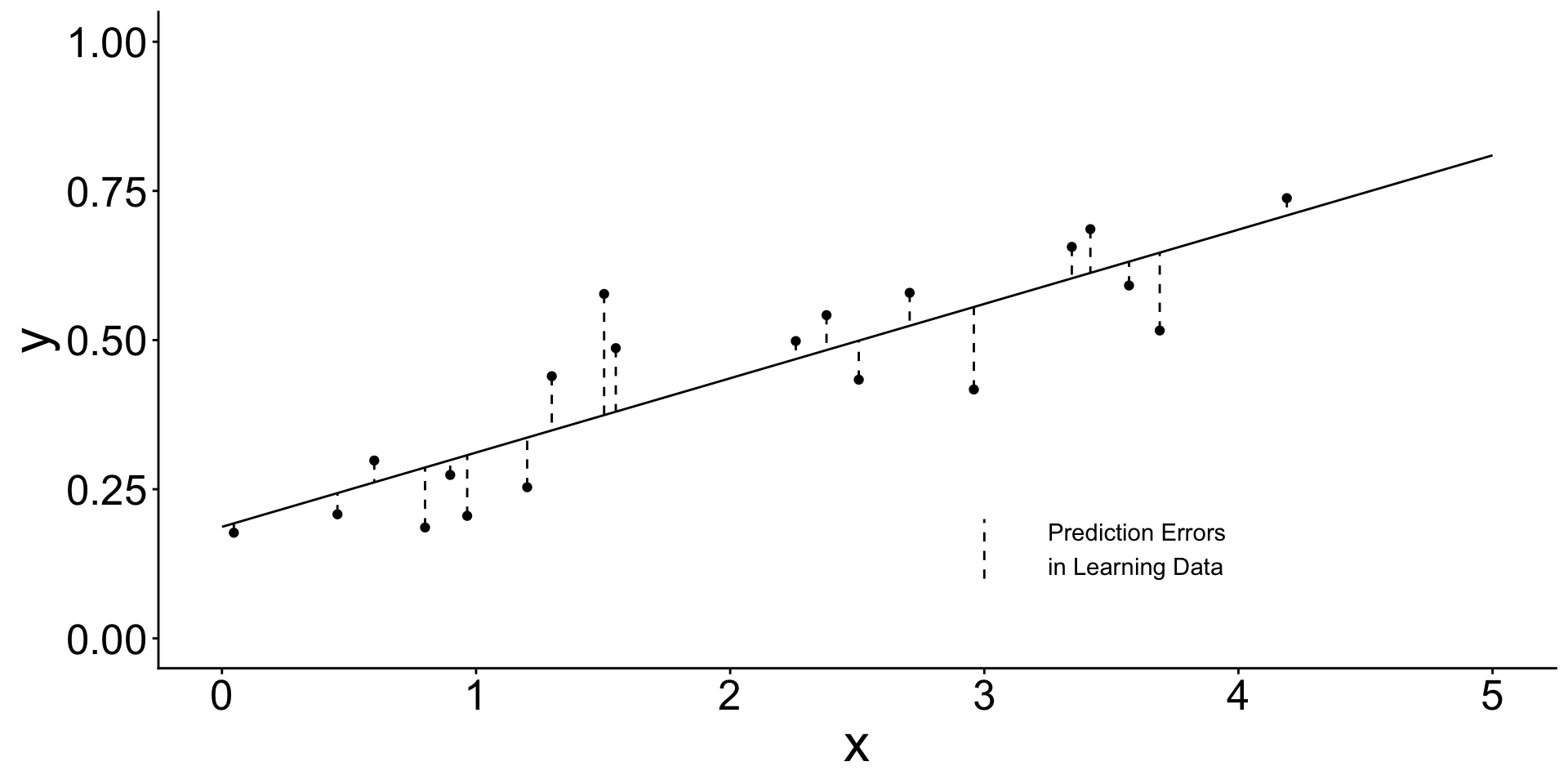

Learning data (used to estimate the line)

![]()

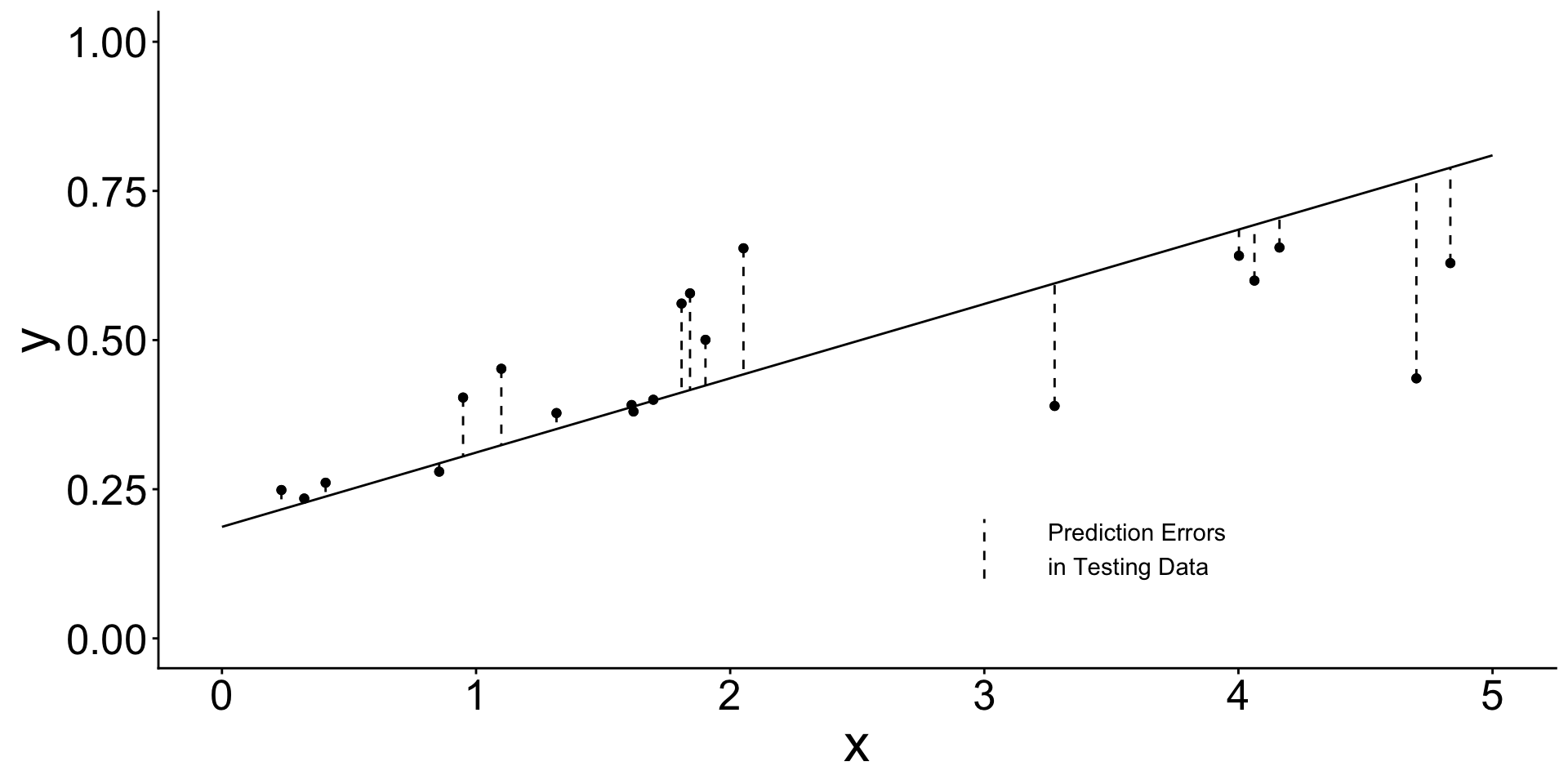

Testing data (used to evaluate the already-learned line)

![]()

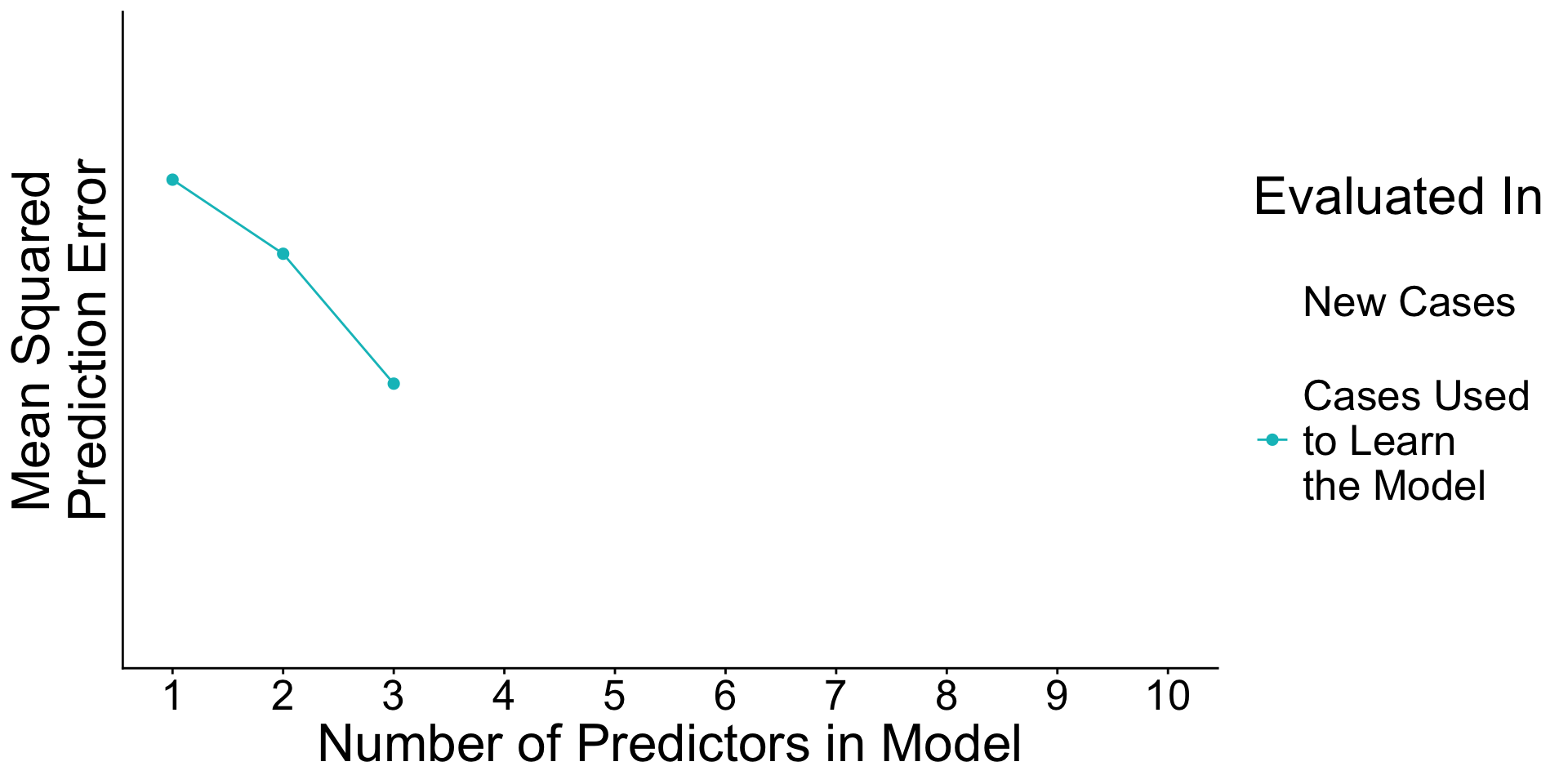

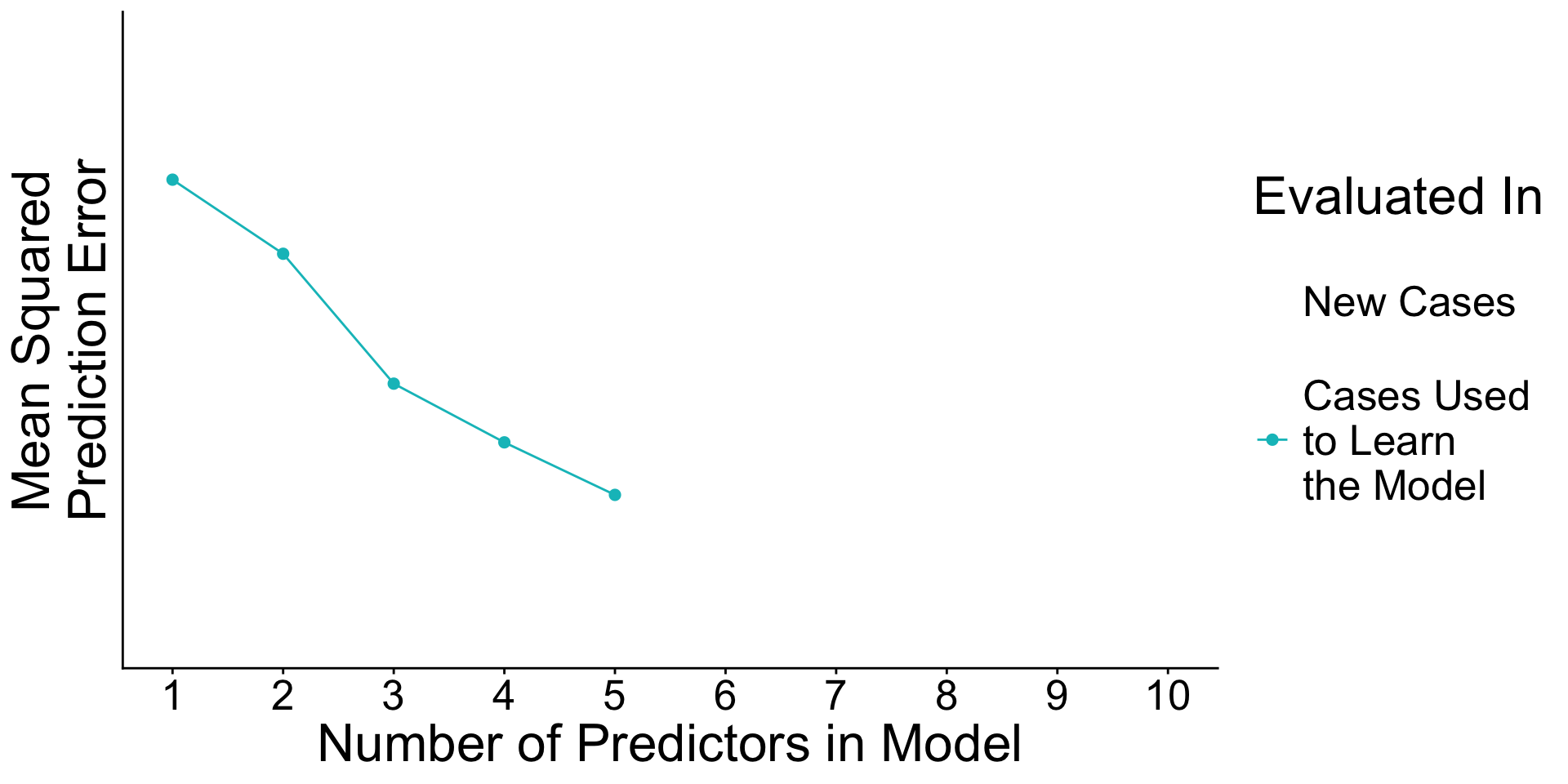

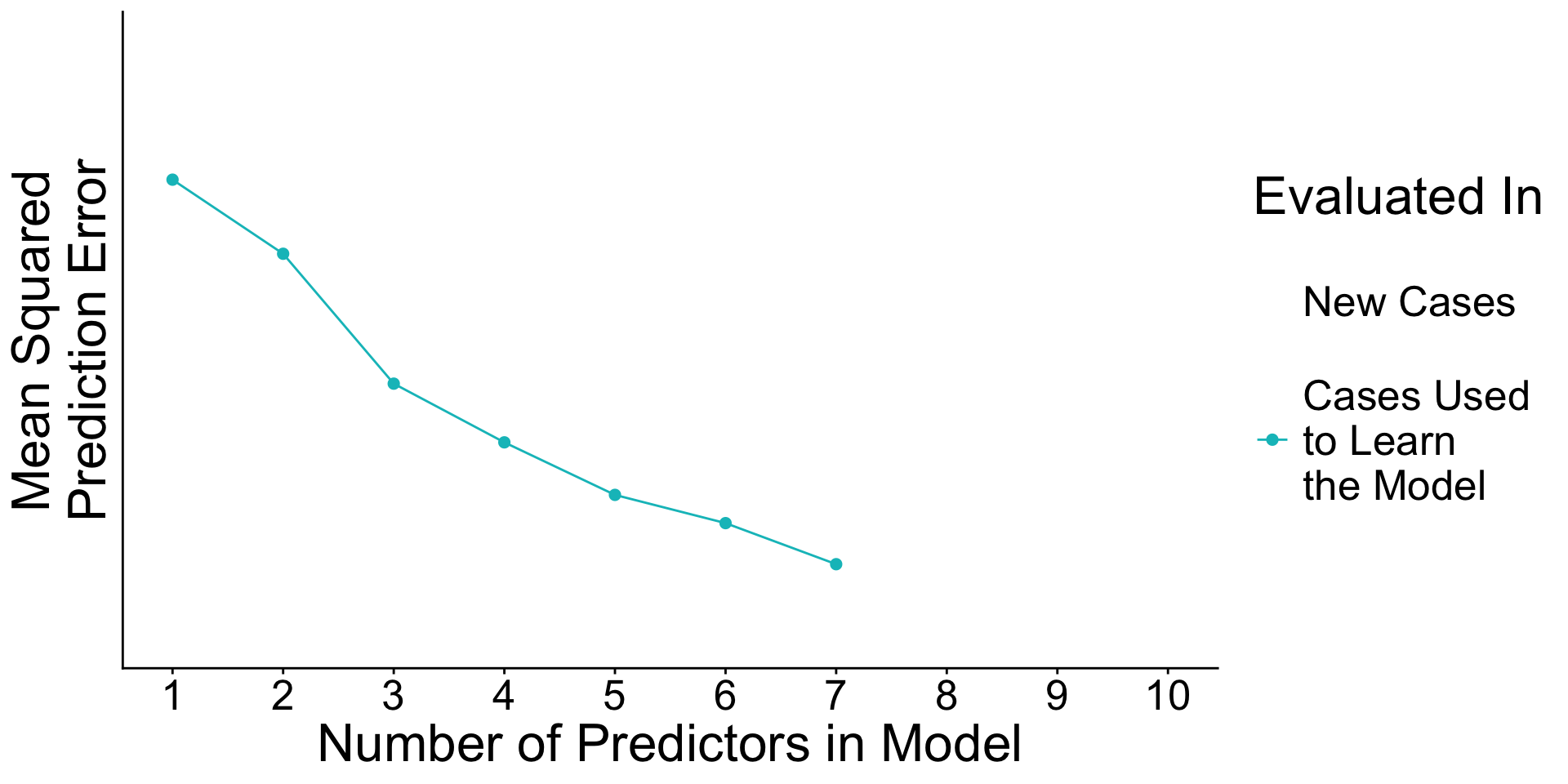

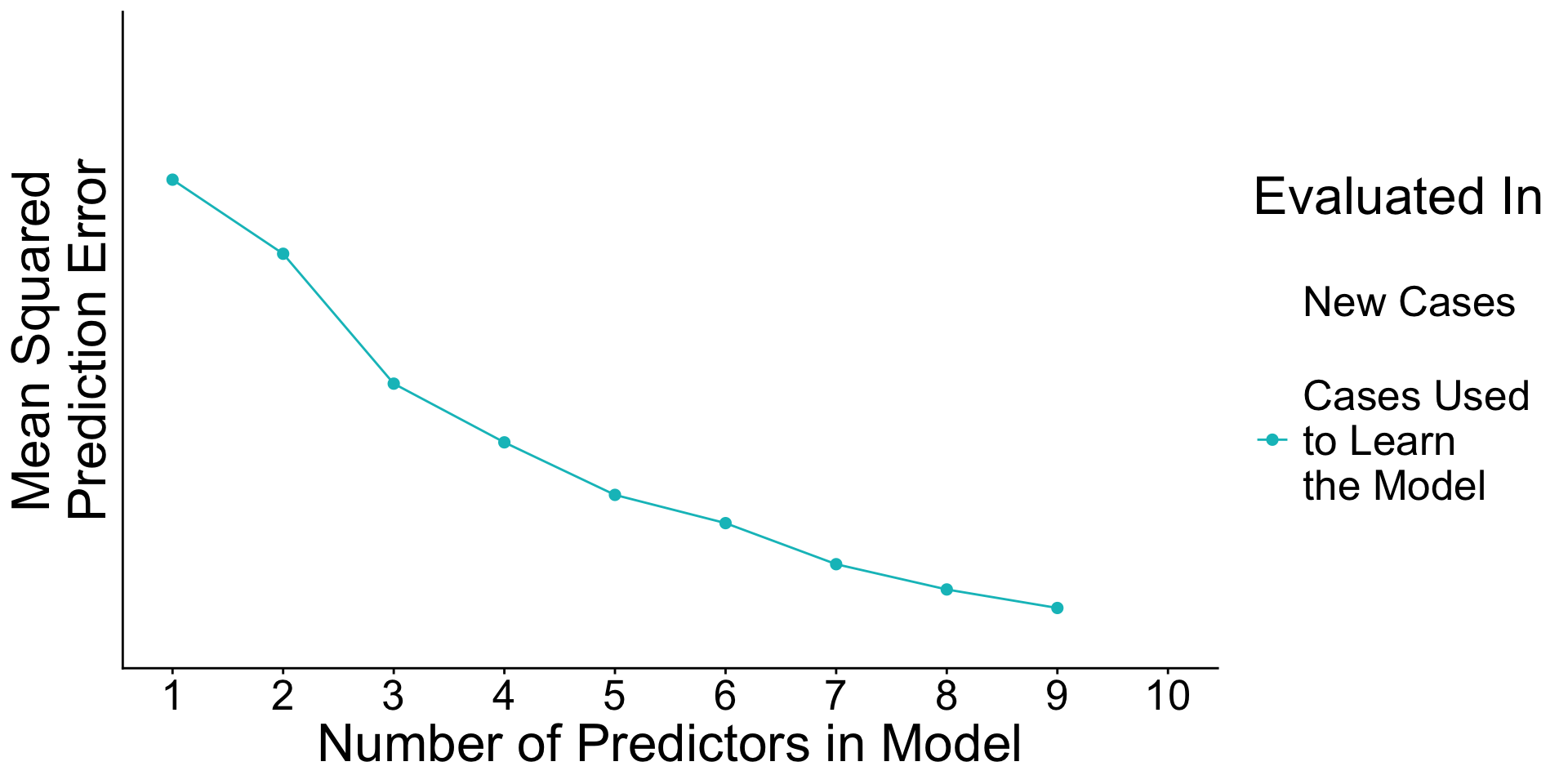

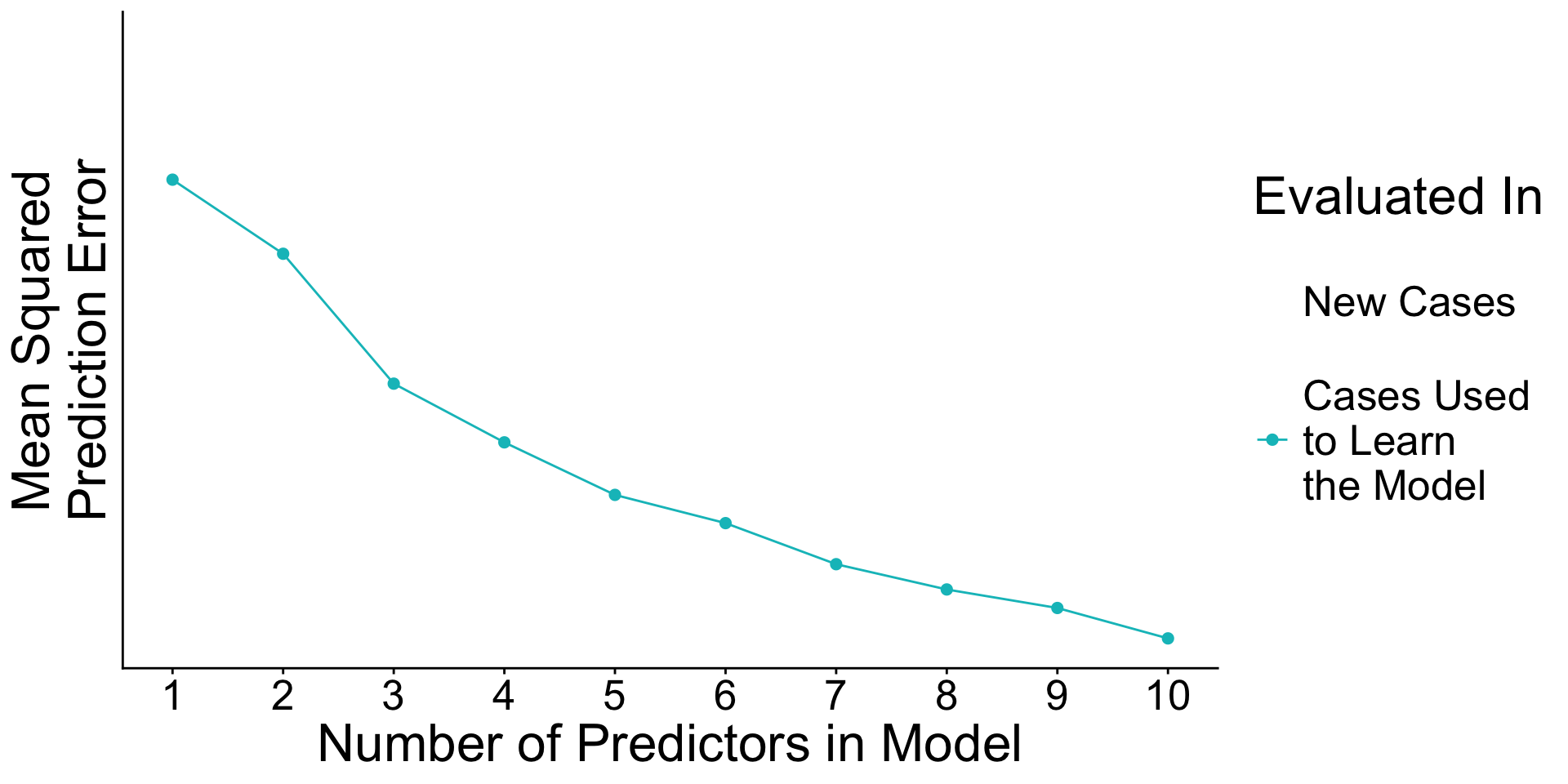

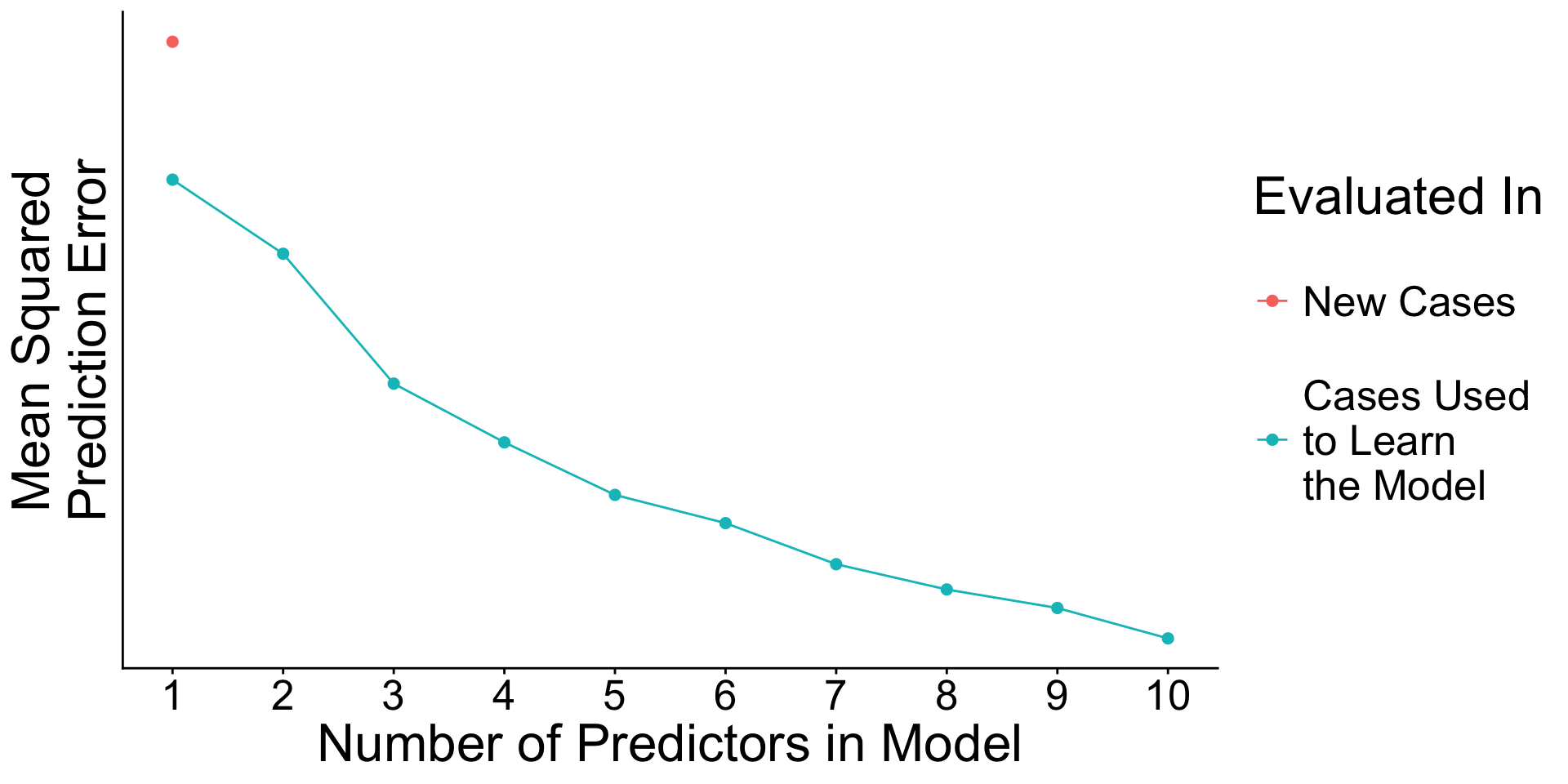

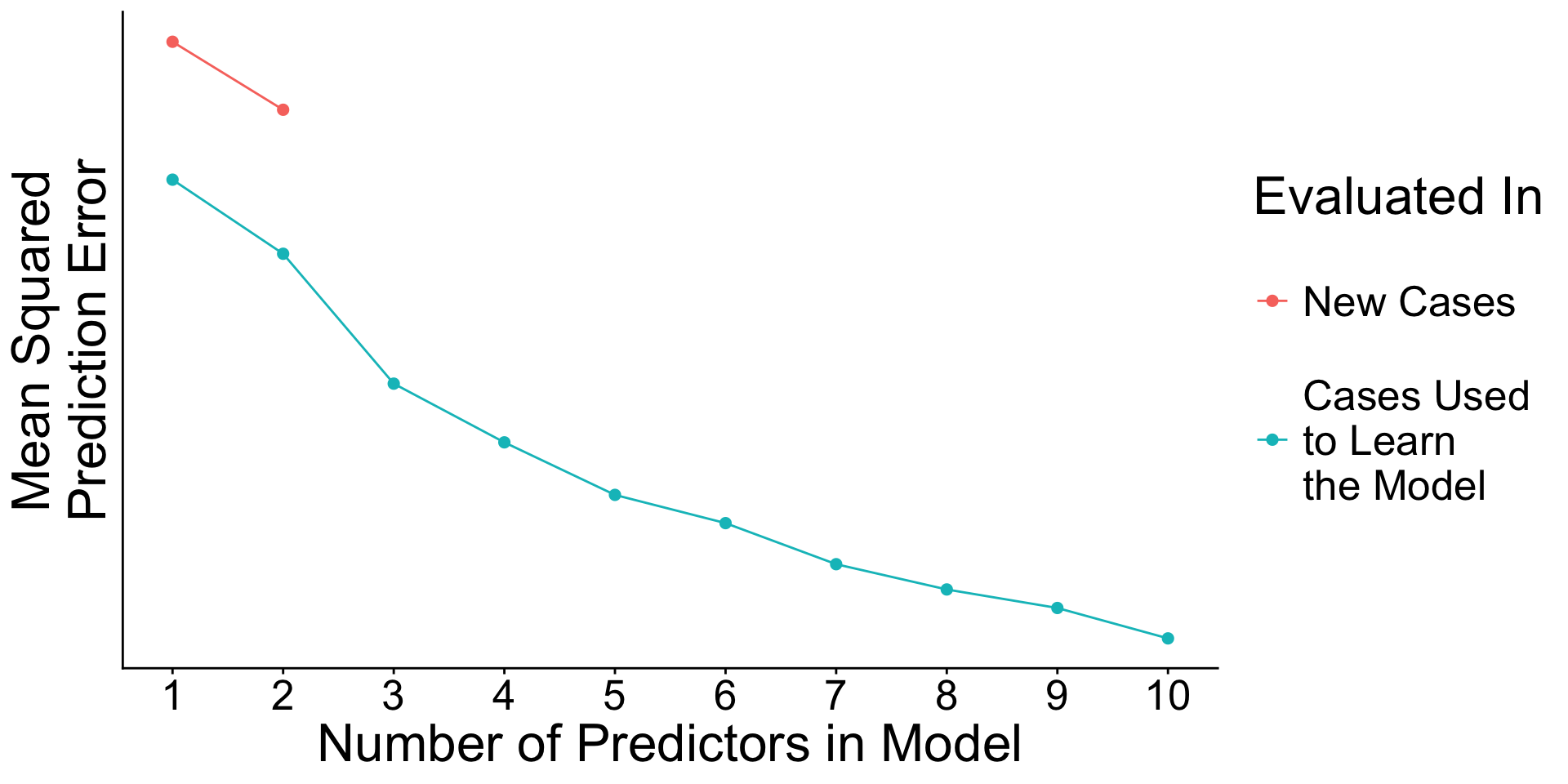

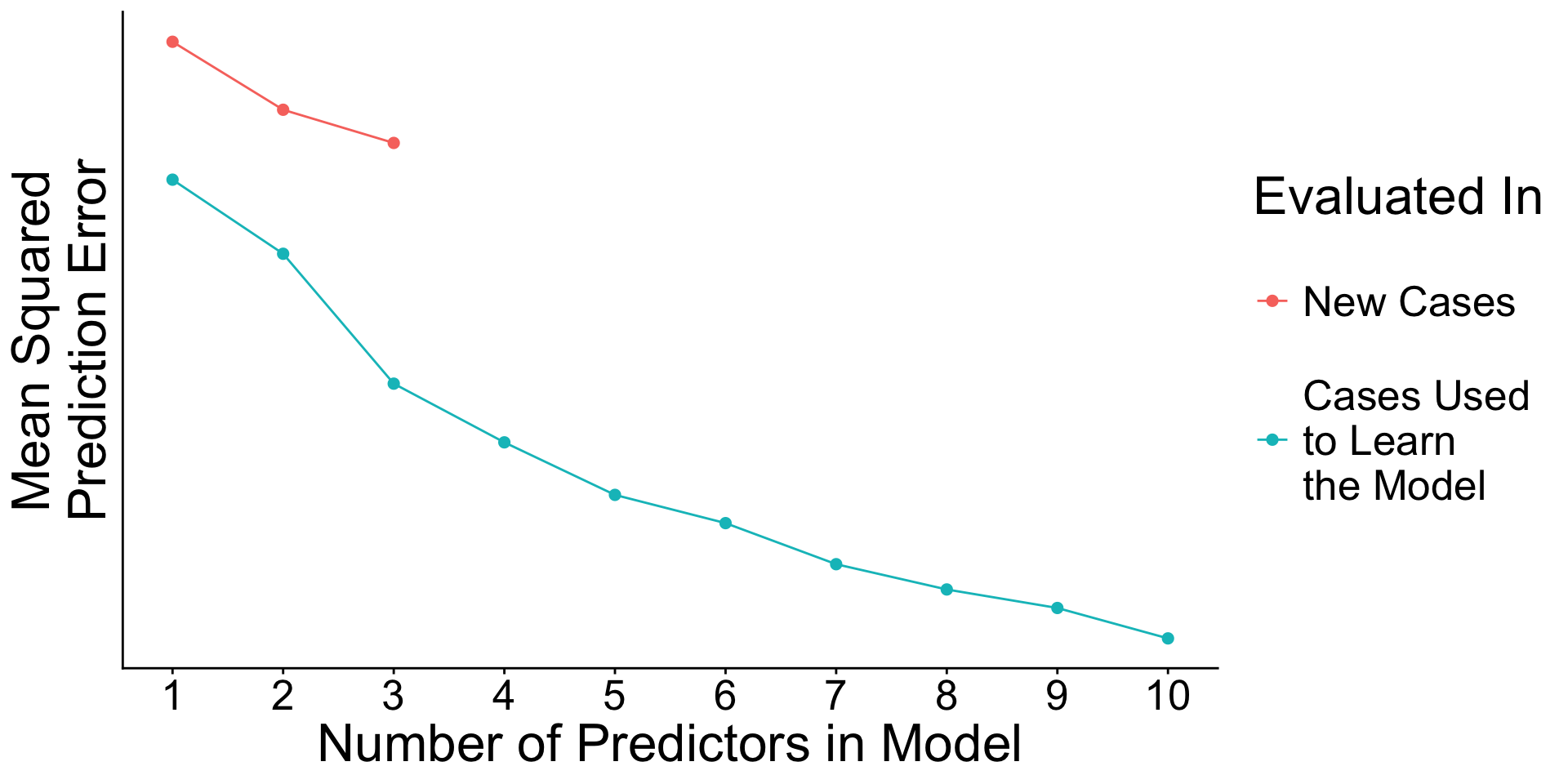

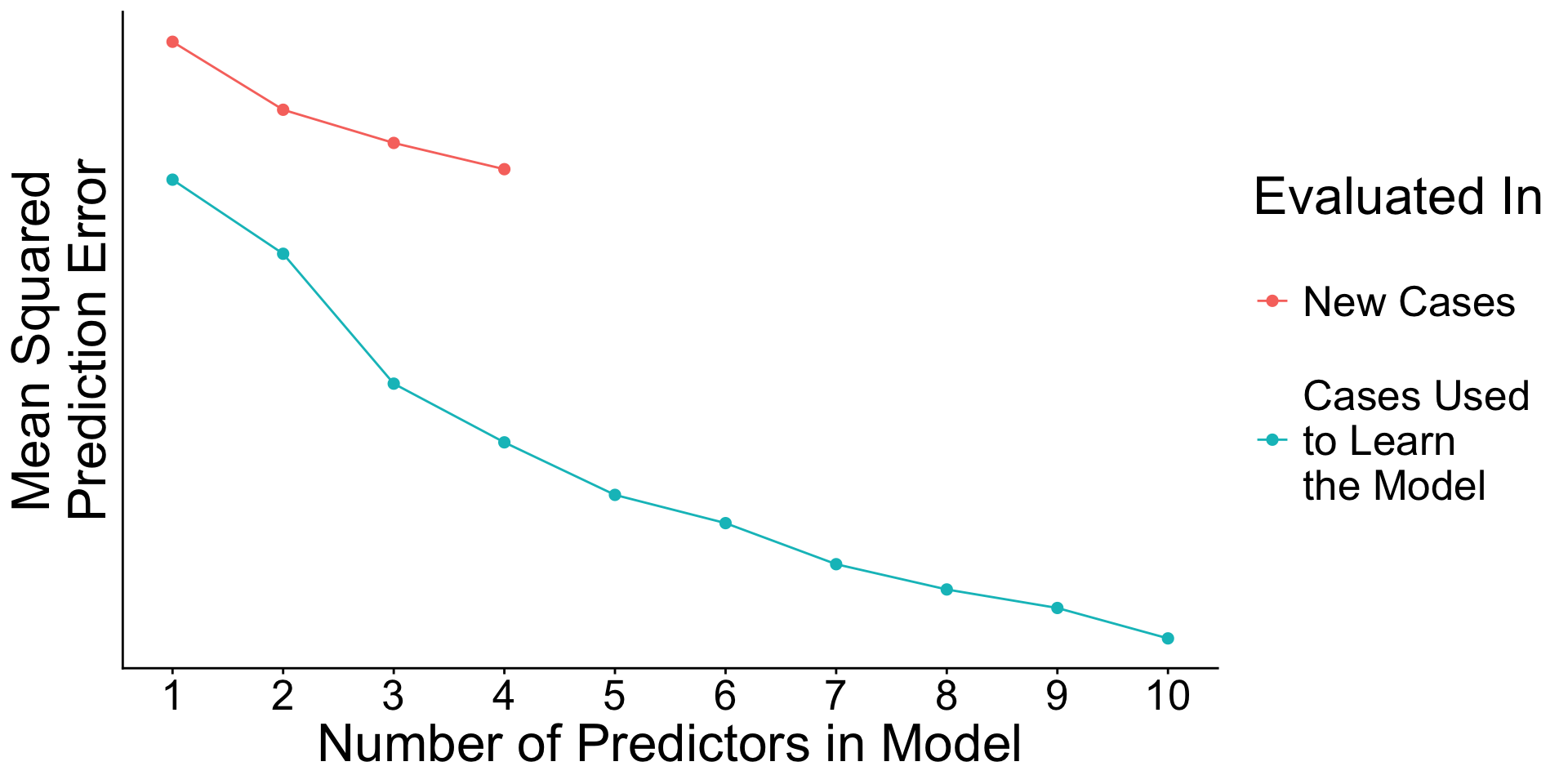

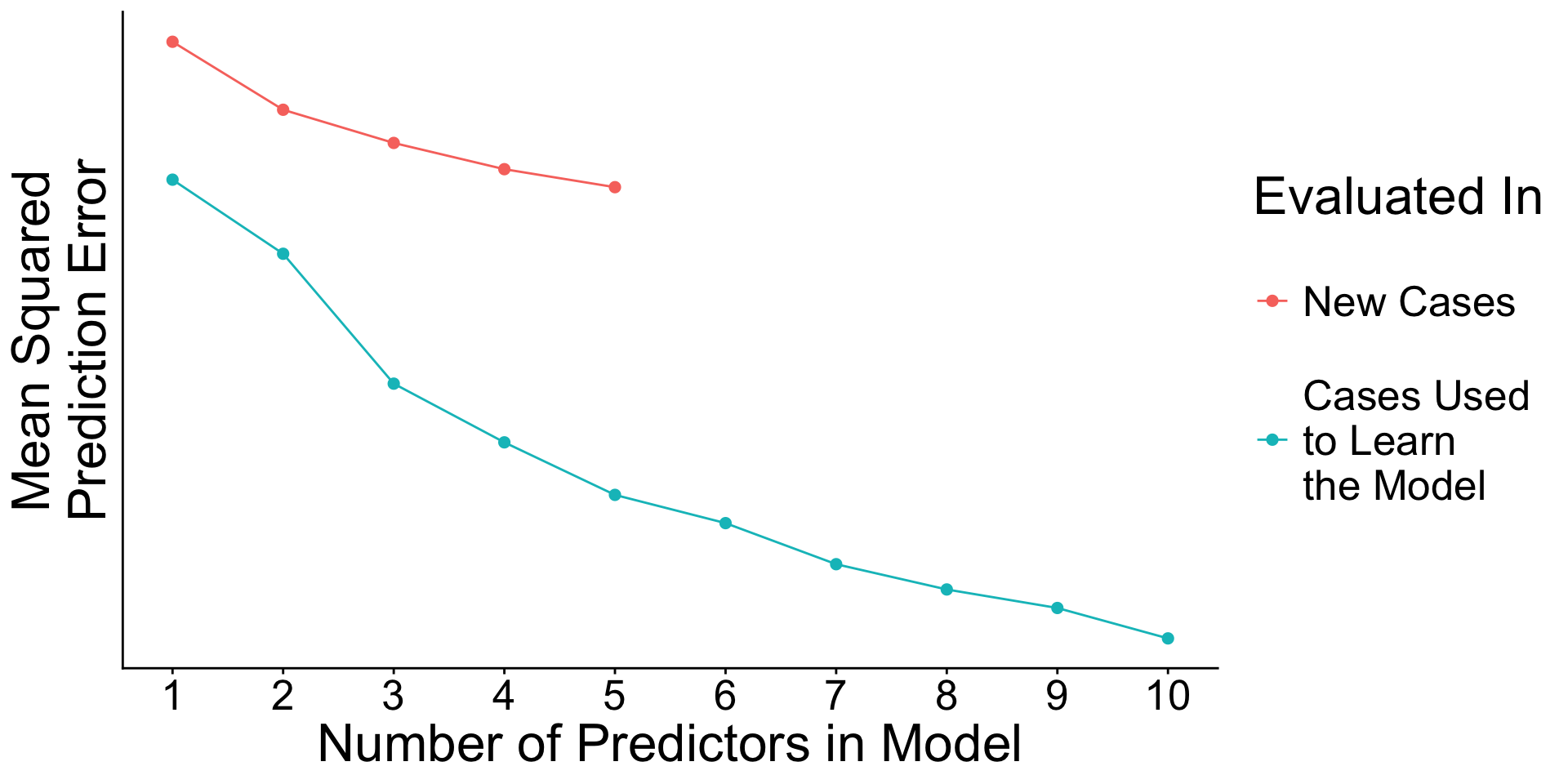

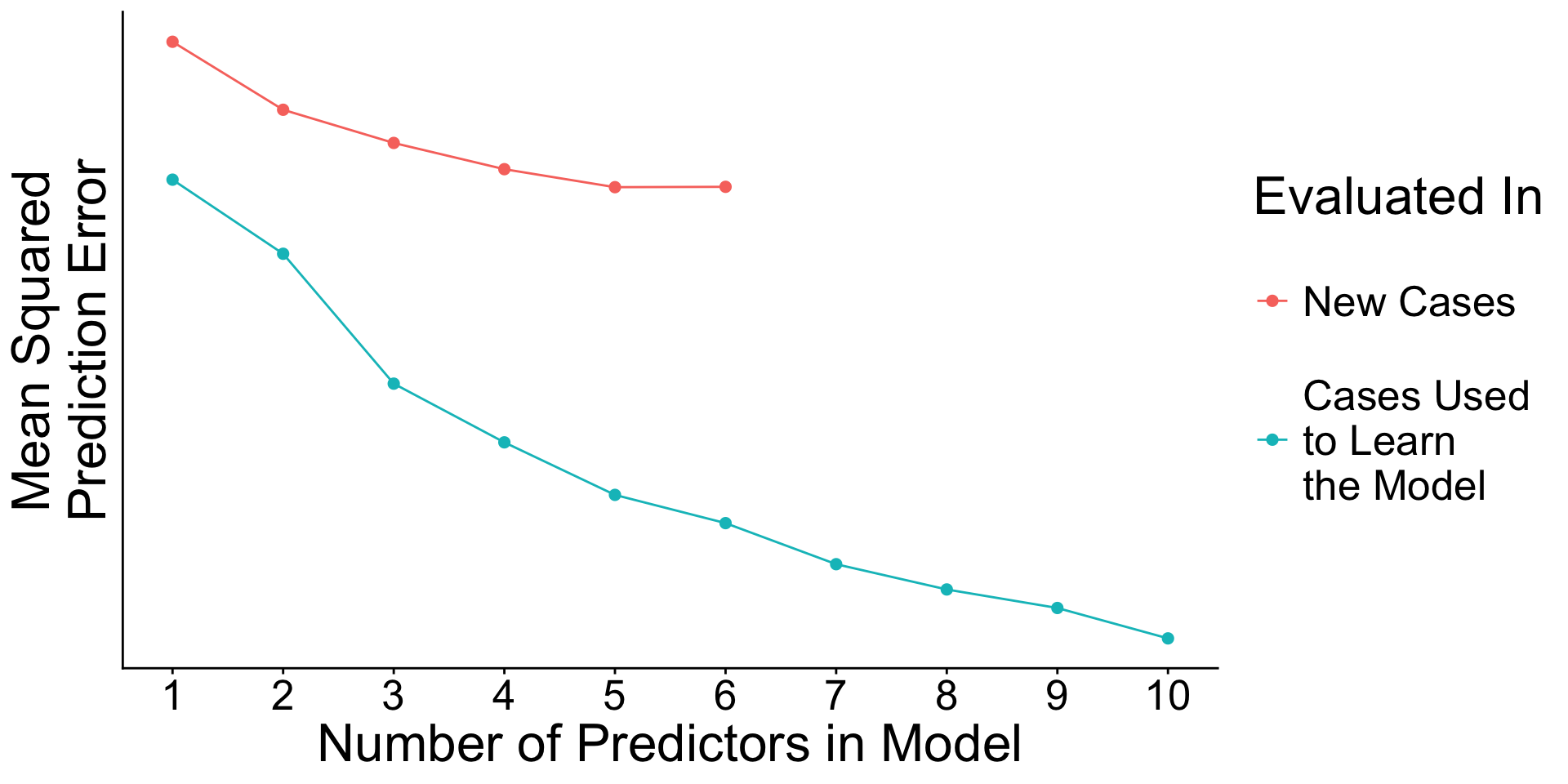

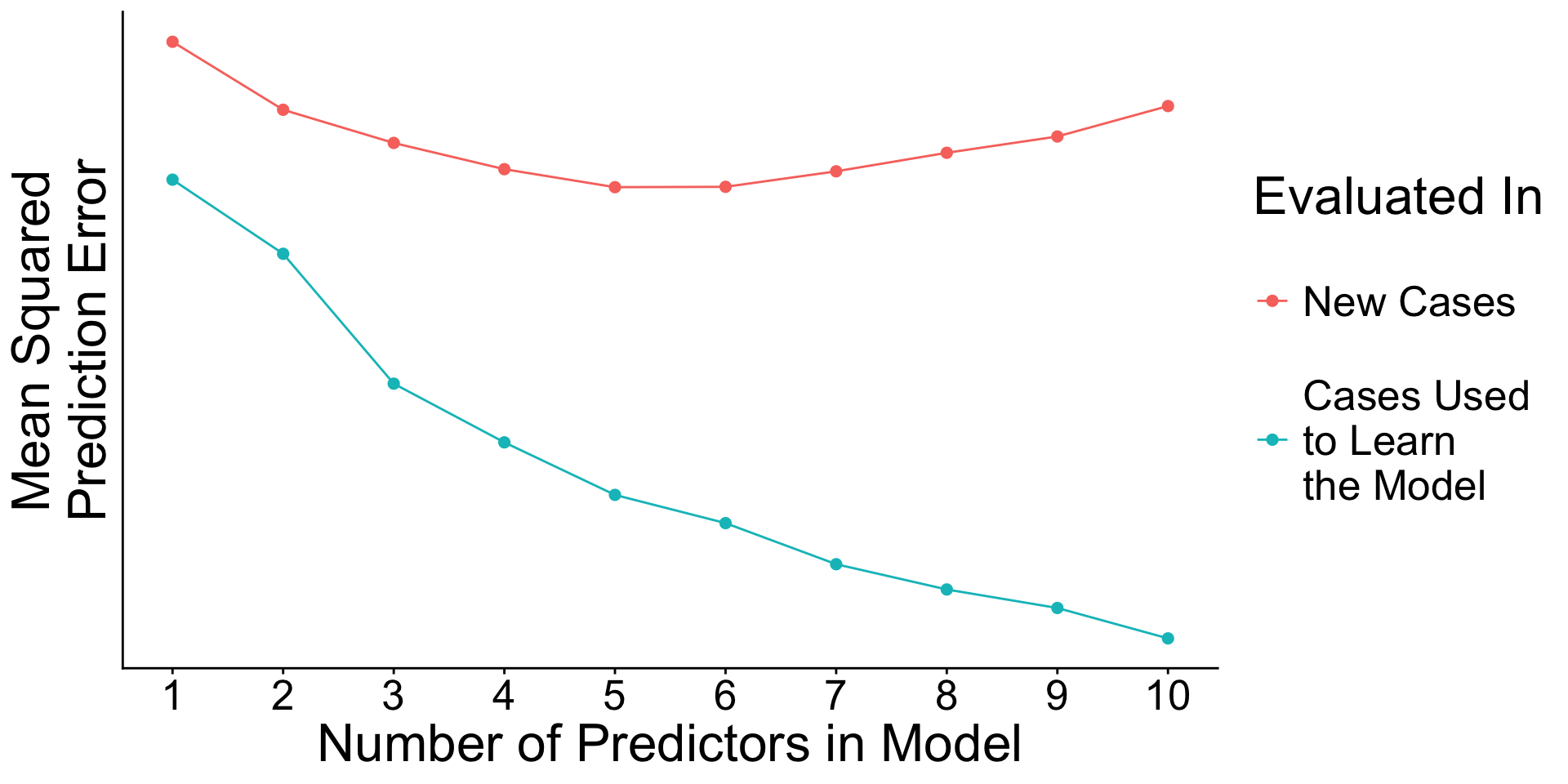

When will prediction errors in learning and testing data differ?

True model:

\[

\text{E}\left(Y\mid\vec{X}\right) = X_1\beta_1 + X_2\beta_2 + ... + X_{10}\beta_{10}

\] with \(\beta_1 = .9\), \(\beta_2 = 0.8\), , \(\beta_9 = 0.1\), \(\beta_{10} = 0\).

We observe \(n = 300\) cases.

Recap: Surprising facts

- An estimated model picks up both

- Signal. True patterns linking \(\vec{X}\) to \(Y\)

- Noise. Random patterns particular to the learning data.

Recap: Surprising facts

- As you add predictors to the model

- error in learning data goes down

- error in testing data may go up

Why? With many predictors, the noise may dominate the signal.

A use case for train and test: Tuning parameters

for_sample_split <- read_csv("https://soc114.github.io/assets/for_sample_split.csv")

- Predictors

x1 through x100

- Outcome

y

- \(n\) = 300 cases

A use case for train and test: Tuning parameters

Recall penalized (ridge) regression. Chooses \(\vec\beta\) to minimize

\[

\begin{aligned}

\underbrace{\sum_i\left(Y_i - \hat{Y}_i\right)^2}_\text{Sum of Squared Error} + \underbrace{\lambda \sum_{j} \beta_j^2}_\text{Penalty Term}

\end{aligned}

\]

But how to choose \(\lambda\)?

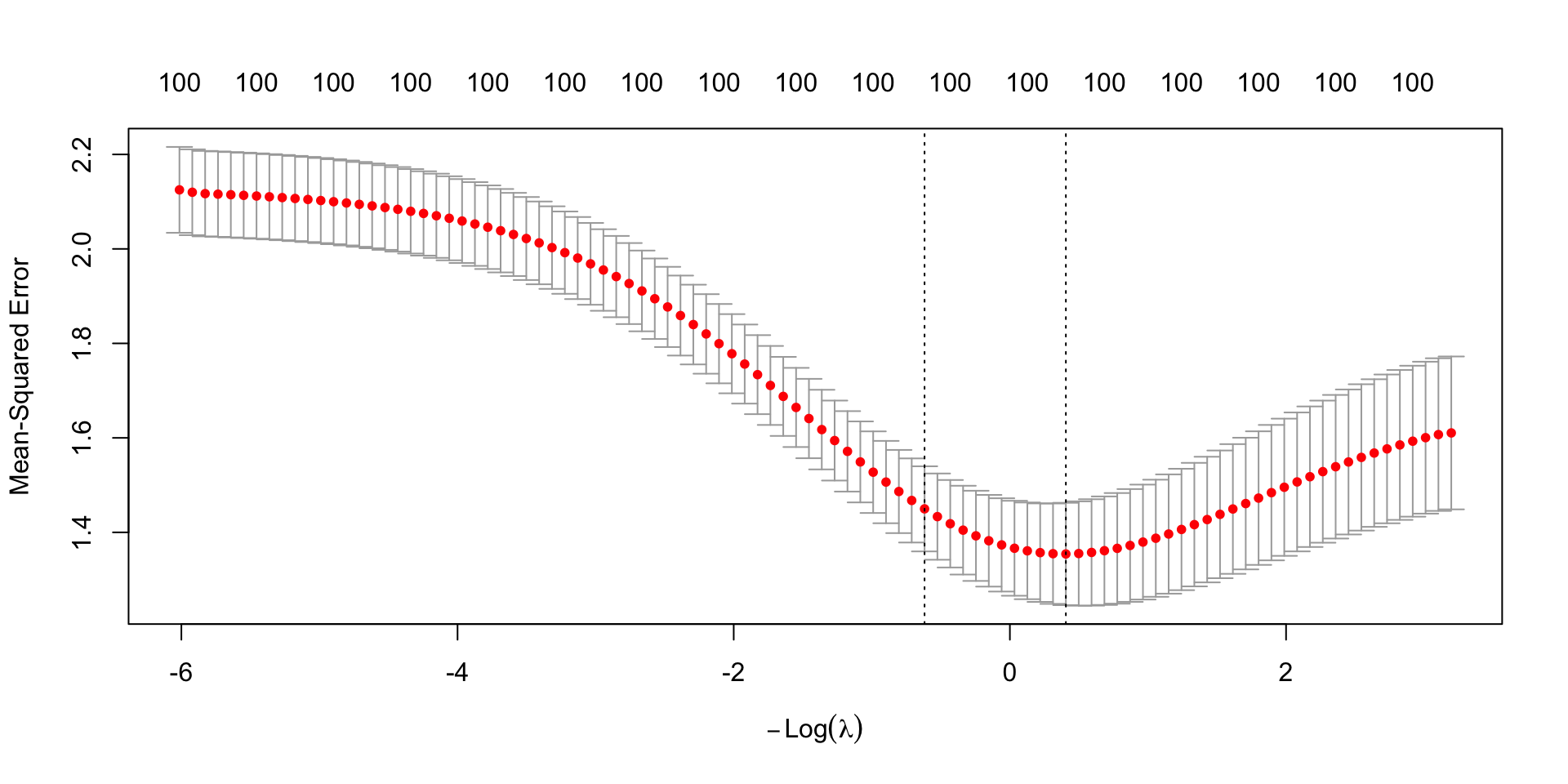

A use case for train and test: Tuning parameters

library(glmnet)

X <- model.matrix(y ~ ., data = for_sample_split)

y <- for_sample_split |> pull(y)

penalized_regression <- cv.glmnet(x = X, y = y, alpha = 0)

cv.glmnet chooses \(\lambda\) for you. How?

A use case for train and test: Tuning parameters

plot(penalized_regression)

![]()

It chooses \(\lambda\) to minimize out-of-sample prediction error.

Recap: Data-driven model selection

When there are many candidate models, you can choose the one with the lowest out-of-sample mean squared error.